Tags

agri-business, correlation, corruption, developed markets, Donegal Creameries, emerging markets, Europe, financial crisis, frontier markets, German property, Japan, portfolio allocation, portfolio performance, QE, US, volatility

Continued from here. Wow, it’s been a leisurely journey – spanning a full year – is this really my last post of the series?! Hmmm, we’ll see… Here’s my portfolio allocation pie chart one more time:

[NB: This is from Jun-2012, but since then the only major changes (funded mostly from my Hedge Fund allocation) are: a) an increase in Property from 10% to 13%, as I continue to scale up my German property exposure (see Parts I to V – also here), and b) a large jump in Agri from 5% to 11%, due to my purchase of Donegal Creameries (DCP:ID) & its subsequent hefty appreciation. Note I don’t classify DCP as an Irish stock – after all, the company feeds people (potatoes, mushrooms & yogurt) and animals, what could offer a more ideal uncorrelated exposure?!]

First, I think one last portfolio overview will provide some valuable context for my final allocation: Once again, it’s worth observing this probably doesn’t look anything like a normal portfolio to many investors! But I can assure you it’s quite intentional, and also pretty representative of my long-term strategy. On average, I’m striving for (say) a 50:50 split between Equities (Emerging & Frontier Markets, UK & Ireland – 42%) on the one hand, and Real Assets, Distressed & Alternative Investments (inc. Cash & Fixed Income) on the other. It’s worth noting my total non-Equity allocation isn’t (necessarily) designed to be low volatility/return. Actually, I’m v happy to accept higher volatility in exchange for higher long-term returns. But it is designed to offer significant diversification, and to ensure a substantial portion of my portfolio enjoys (ideally) a low, neutral, or even negative correlation with the market & the economy.

[Admittedly, this lack of correlation is somewhat of a pipe-dream…at least in the short-run. To explain: My non-Equity investment theme(s)/allocation is mostly created via listed equity investments – and when markets crash, we unfortunately re-discover pretty much all equities crash, regardless of their underlying fundamentals or lack of correlation. However, I’m confident the benefits of this allocation approach can be realized in the long-run].

My allocation is somewhat skewed right now against Equities. Mostly because I’m happy to ignore benchmarks & omit vast swathes of the (developed) world from my portfolio…like Japan & the US! Of course, this is probably a little silly – obviously, QE is usually equity-friendly, but I find it damn hard to invest in countries where I dislike the underlying macro & currency fundamentals. Particularly when they appear to be taking a turn for the worse…

I also have to wonder what’s priced in at this point – N America began the year as one of the more expensive regions in the world. And I’m stunned to note the US (neck & neck with Japan) is one of the lowest yielding markets in the world. [Er, let’s not even mention that pesky CAPE ratio…] So, if the US economy starts to boom, how much of that’s already discounted & how will investors react to the Fed’s attempts to reverse QE? In fact, we may be seeing a taste of that right now… But what happens if the US falls at the next hurdle? Well, obviously everybody will still cling to QE as a crutch, but how long can they continue to ignore the underlying fundamentals, or ever diminishing short/long-term returns from monetary/fiscal stimulus?

Of course, Europe basically faces the same issues, but much of the continent is priced far more cheaply. And the decades-long record of the Eurozone hard-core suggests the Euro will remain the least dirty shirt in the developed world. In my opinion, Ireland’s labour flexibility & the UK’s currency/monetary flexibility make them the obvious low-risk play on Europe (& Scandinavia may offer more of the same).

OK, now let’s home in on the remainder of my Equity allocation…

Emerging & Frontier Markets (23%):

You’ll immediately note well over half my Equity allocation (of 42%) is devoted to Emerging & Frontier Markets – which is v deliberate. [Imagine I had a zero non-Equity allocation – I’m confident Developed Markets would still comprise less than half my portfolio]. Because we’ve now reached a cross-over point – looking ahead, emerging/frontier markets’ collective GDP will surpass that of developed markets. [Nicely illustrated by a recent Bain report which confirms the Chinese have now become the world’s top luxury goods spenders!]. Simply taking a neutral benchmark perspective (based on GDP), half of every investor’s equity portfolio/allocation should now be devoted to emerging/frontier markets. In fact, if you consider their far more attractive pricing & growth prospects (vs. developed markets), wouldn’t an overweight position actually make perfect sense?

So…how does your portfolio look?!

Honestly, I’ve only ever come across a handful of investors online, or in person, who have a deliberate & significant allocation to emerging/frontier markets in their portfolios. That’s quite astonishing – and depressing – maybe I just know the wrong people… Perhaps pension & retirement funds, or adviser portfolios, are there to take up the slack? Er, no… Christ, have you looked at the average pension fund recently? Seems like they’ve come full circle in the last couple of decades – they’re chock-full of home bias & bonds, I simply shudder at the thought.

[Another terrible example of the wants of the Baby Boomers f**king over the next generation. I mean, picture you’re a 30 yr-old who’s lucky enough (these days) to have a pension – considering your time horizon, a 100% allocation to emerging/frontier markets might be a perfectly rational choice, yes? But check the label on the tin, there’s nothing remotely like that in your pension fund… Dare I suggest pension funds should be tranched?!]

But maybe you should be excused – perhaps you have one of those insidious emerging market nay-sayers always whispering in your ear? I call them developed market douche-bags. The kind who always have a persuasive & intelligent argument why emerging markets are dangerous, why they’re just about to crash, and how they should be avoided like the plague – like right now, I guess..!? For these folks, it doesn’t matter if developed markets are ready to boom or bust – and it really doesn’t matter what year it is either, emerging markets are always bad news! [And for God’s sake, don’t mention frontier markets – they’ll just start foaming at the mouth!] Except, except…do I really need to point out how spectacularly & ridiculously wrong they’ve been over the years?

And seriously, we’re talking about well over a decade here – don’t let them tell you this chart’s just bad luck (?!) & they’ll be eventually proved correct. That’s like Bernie Madoff saying his numbers will come right in the end! Aaah, that was fun – let’s have a do-over, and add some bells & whistles this time:

Yup, that’s pretty definitive…

Oh, and sad to relate, but that shit developed markets performance (over the past dozen years) doesn’t even include the US (which clocked an even shittier CAGR of 1.9%). Of course, the past is the past – those charts could prove a terrible siren-song if they simply reflect a massive multi-year revaluation of emerging/frontier markets. But c’mon, you know that’s actually not the case..!

In the end, I just can’t shake the suspicion emerging/frontier markets are like religion or politics for a lot of investors. You’re either pro- or anti-, and nothing will ever change that opinion. And I certainly wasn’t planning to cast myself as an evangelical cheerleader for emerging/frontier markets either! Ultimately, I believe everybody has to invest on the strength of their own research & convictions. But crikey…I just can’t resist! 😉 I’m sure I can quickly bang out about a dozen compelling long-term reasons to prioritize investing in emerging/frontier markets:

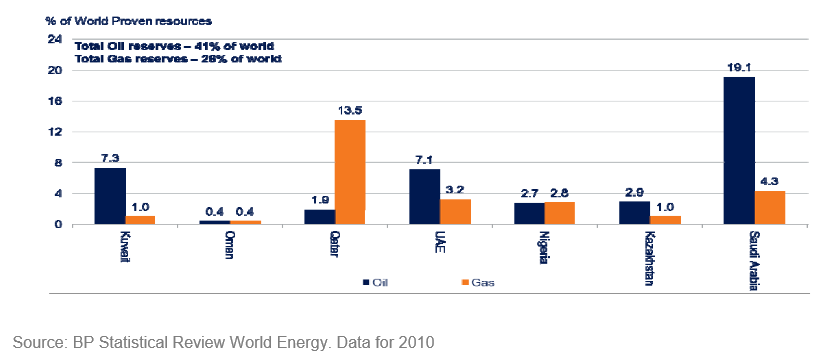

– Natural Resources: Emerging markets enjoy an abundance of natural resources, while frontier markets (despite their currently small share of global GDP) possess over 40% of the world’s oil reserves & over 25% of its gas reserves

– Labour Costs: Emerging market labour costs are a mere fraction of developed market costs, while in turn frontier markets also enjoy a fraction of emerging market costs

– Demographics: Emerging/frontier markets have far younger populations – in fact, almost 60% of the population in frontier markets is under 30 years of age. The limited provision of health & retirement entitlements in many of these markets is another great tail-wind they’ll enjoy

– GDP Growth: In the 5 yrs from 2007, emerging/frontier markets averaged 4-5 times the GDP growth rate of the developed markets. For the following 5 yrs (from 2012), they’re still expected to produce nearly double the growth of developed markets

– Debt-to-GDP Ratios: Just look at that bloody graph! Wow…and the gap probably just gets worse from here

– Correlations: While emerging markets continue to suffer rising correlations, frontier markets offer low correlations to both developed markets and emerging markets

– Market Cap as % of GDP: Listed equities in emerging/frontier markets represent a substantially lower percentage of the economy. As countries develop & incomes/prosperity improves, history indicates that companies & entrepreneurs will boost the supply of equity, which will be met by a growing wave of domestic investment demand

– Relative Performance: YTD, emerging markets have suffered a double digit mark-down, while the US (for example) has enjoyed a double digit return. Despite continuing strong economic & earnings growth, frontier markets remain far off their 2008 highs & have significantly under-performed emerging markets

– Pricing: Emerging markets began the year on a 13.1 P/E, a slight discount to a shell-shocked Europe & a significant discount to the 15+ P/E enjoyed by N America. Frontier markets traded on just a 10.7 P/E, a substantial discount to pretty much all markets globally. And it would surprise many to learn emerging market investors enjoy a better dividend yield than those in N America, while the 4.2% average dividend yield frontier markets are sporting is one of the best in the world!

Finally, there’s some weary old canards the developed market douche-bags always like to trot out…

– Volatility: Let’s not get all emotional – they can just look back to the return charts I posted above, it’s all there in black & white. Sure, emerging markets were about a third more volatile over the years – but so what, one earned 3-4 times what the developed markets clocked up! Ignoring that kind of risk:reward equation is simply their loss… As for frontier markets, I’m speechless – only an idiot would want to pass up the highest of returns & the lowest of risks!? Anyway, where were these people in 2008 – hiding out in the developed markets? I hope they bloody enjoyed that particular brand of volatility…

– Corruption: Oh please, hold my sides…they’re splitting! Corruption hasn’t disappeared in Western markets – it’s just become more sophisticated & expensive. I mean, how else do you explain the trillions being lavished right now by politicians (& central banks – who’ve been reduced to political slavery) in Europe & the US? No wonder lobbying is justifiably identified as offering the highest return on investment…ever! That kind of stuff makes the corruption found in emerging/frontier markets look like penny-ante shit!

OK, now we still need to think about different approaches to investing in emerging/frontier markets, and I have a bunch of stocks for you to consider as potential investment opportunities. You know what…why don’t we keep all that for one more last gasp post in the series?! 😉

To be continued…

btw Here are some (fairly recent) primers on frontier markets that you might find interesting/useful:

http://www.everestcapital.com/Observations/Observations.aspx

https://pressroom.vanguard.com/nonindexed/1.18.2013_Exploring_the_Next_Frontier_Equity.pdf

Pingback: Quite A Saga… | Wexboy

Pingback: Portfolio Allocation (XV – Emerging & Frontier Markets) | Wexboy

The first thought that comes to my mind is GDP growth does not necessarily correleate with share price growth.

I was a big bull on China for awhile but look at the results, since 1990 the main chinese stock index has only doubled. 23 years of growth and it has doubled, that is maybe 4% per year plus dividends.

If you are not careful, corporate fraud and mismanagement can easily swallow all the growth.

That chestnut…perhaps I’m wrong, but if I recall, those studies were limited to developed markets – where GDP growth has progressively compressed & converged over the past years/decades. Which makes it nigh impossible to meaningfully correlate market performances with respective GDP growth levels (the same is even more true for bilateral FX rates). The other obvious reason is that investors generally price in a market’s prospects, which tends to be a great equalizer also. At the end of the day, price always matters, even with emerging/frontier markets – higher GDP growth won’t necessarily bail you out if you blithely over-pay.

Corporate fraud & mismanagement – I presume you mean US real estate/mortgages & the ensuing credit crisis? Yes, I agree…

Interesting to see Mark Mobius making many of the same points in favour of emerging and frontier markets in the FT on the same day you posted this!

http://www.ft.com/cms/s/0/efa289c2-d995-11e2-98fa-00144feab7de.html

Yup, I sent him a cheat sheet…OK, only kidding 😉 Yes, Mobius is still a great champion of emerging markets (far better than Marc Faber – God knows what he might come out with in an interview!), and I’m delighted to see he & Franklin Templeton placing an increasing emphasis on frontier markets these days.

I am always fond of the emerging and frointer markets. Enough that I decided to put £1200 in the Neptune Africa Fund which I am not entirely sure it count as Emerging Market as it is mostly in South Africa. Nevertheless, it is my belief (entirely unbiased belief) that Africa will do well in the very long term. (I am only 27 so I can afford to wait for few decades!)

But if you are talking about shares, then I guess out of my portfolio, Auhua Clean Energy (based in China) and Graphene Nanochem (based in Malaysia). Although Eden Research does a deal with an articultural company in Kenya which may yield some revenues.

If you include my one off investment in some Africa Fund and my own portfolio (Chinese and Malaysian companies), then it make up tad over 25% on cost basis.

I guess you are more into general market rather than specfic countries I guess.

I am seriously looking forward toward your next post with potential consideration and of course, your rather amusing tone of writing.

Thanks, Joe – that’s a good allocation to start with! Yes, I also think Africa’s reached an important inflection point – I’ll expand on that a little more in the next post.

Appreciate your posts, what would be your recommendations regarding ways to play frontier markets? Thank you.

Cheers Peter,

As with the rest of this series, I don’t plan to make specific recommendations, but in my final (upcoming) post I do hope to suggest a few different approaches to investing in emerging/frontier markets, and offer up plenty of stock ideas at which you can take a closer look.

Id be v interested to get your view on OPP LN(Origo partners). A Private Equity focused on resources. It is starting to play Myanmar and has been in Mongolia for a few years. Price action terrible but wondering if there’s any value there. Thanks a million- Love your work!

Thks Shane,

OPP unfortunately suffers a real trifecta of hate right now: China, Mongolia & natural resources, ouch! However, it now trades on a 0.25 Price/Book – it becomes a lot harder to lose money on a stock like that, unless management’s actively engaged in destroying value. I don’t think that’s the case here – they’re just stuck in a shitty investment sector. But prospects & sentiment can/will change in due course, and the price offers some good defence meanwhile – the new Myanmar focus is tres trendy, but perhaps quite promising from a private equity perspective.