Tags

Botswana Diamonds, Brexit, Connemara Mining Company, Dalata Hotel Group, GAN, Green REIT, Irish shares, Irish Stock Exchange, Irish value investing, ISEQ, Mincon Group, New Ireland Fund, TGISVP, The Great Irish Share Valuation Project, UDG Healthcare

Continued from here.

Apologies, I abandoned TGISVP for a few months there…dealing with a mild case of PBSD. Yes, I mean Post-Brexit Stress Disorder, which I suspect the entire island’s been experiencing too! Dare I say it, Ireland’s officially the kids in this bloody divorce – did Brexiteers ever stop & consider them when they were voting? Which begs the question:

What did they really think they were voting for..?!

Noting the 51.9% final tally for the Leave vote, we can presume a distinct minority of the population specifically voted for Hard Brexit. And yet, that’s what the UK now seems to be getting. [Again, when the Tories voted for Theresa May, what did they really think they were voting for..?!] But maybe it was inevitable…by default, Remainers now favour a Soft Brexit, which unfortunately seems to have persuaded the entire Leave campaign they believed in Hard Brexit from day one. And that’s what we’re seeing reflected in May’s government, which on occasion appears to have swung even to the right of Enoch Powell, and where Hammond & Carney were even branded traitors for simply highlighting some of the inevitable fiscal/economic consequences of a (Hard) Brexit. And anyway, the Soft Brexit peddled by the Leave campaign was sheer fantasy – no open borders (except the Irish border!?), no nasty EU-type regulations, free trade into the EU, jobs for all, etc. – basically, you can have your cake & eat it too (ooh la la, that’s a bit French!). In the end, it’s hard to know which was worse – the cynicism of the Leave campaign, or the gullibility of millions of Brexit voters who swallowed it hook, line & sinker…

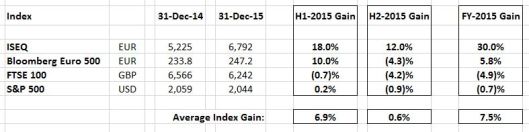

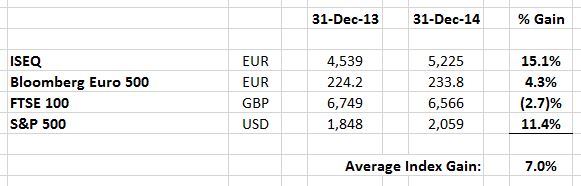

But anyway, despite May’s current stance, we’re really no better informed than we were in the aftermath of the referendum, and it will be a few years down the road (possibly with an additional transition period) before a new Brexit reality’s nailed down properly. [And never under-estimate the possibility of another referendum!] Which means it’s still nigh on impossible to evaluate the potential future impact on Irish companies & the economy – overall, my (generally positive) perspective on Brexit hasn’t changed much since July, with the EUR/GBP rate still presenting the primary medium-term challenge. [Fortunately, the rate’s back within a percent of July levels, after hitting 0.9100+ in October]. But as I’ve highlighted before, Irish companies have actually proven themselves time & again over decades of Irish-UK exchange rate volatility. And looking at a longer term chart, today’s rate isn’t all that extraordinary anyway: